Markets continue to be volatile, reacting to every new bit of information; large daily moves have become the new normal. Read our previous market update to learn more about it.

Concerns continue to centre around inflation (market looking for signs that it has peaked), as well as Central Bank policy responses, trying to glean whether the hiking cycle will be more or less aggressive than currently being projected and whether these new implications would make a recession more or less likely.

Our standard quarterly commentary will be written early next week and will cover our latest macroeconomic thoughts and portfolio and fund performance in detail.

Therefore, we thought it would be more beneficial to our investors not to duplicate efforts. Today we would write about something more thematic; dividends & income and the role they play in your portfolio.

Dividends – A balance between yield and growth

Most assume that a high dividend yield in isolation is a good thing, but this is not always the case. Dividends are a way companies return monies to shareholders, usually paid out of net profits. However, paying a dividend to shareholders comes at a price, with the company forgoing the opportunity to reinvest to stimulate future growth.

In some instances, this can signal a lack of suitable future projects from which to achieve this growth.

In one basic example, paying high dividends (compared to net profits) for a sustained period, combined with a lack of reinvestment into the company, could lead to a loss of market share and therefore reduce earnings and profits.

Over time, as earnings reduce, dividends would need to be cut, also to the detriment of the company’s overall market value. However, we understand client needs for income but would also emphasise that a balance between yield and growth is preferred over the long term. Therefore, we prefer to use fixed income strategies rather than purely equity strategies to achieve higher yields.

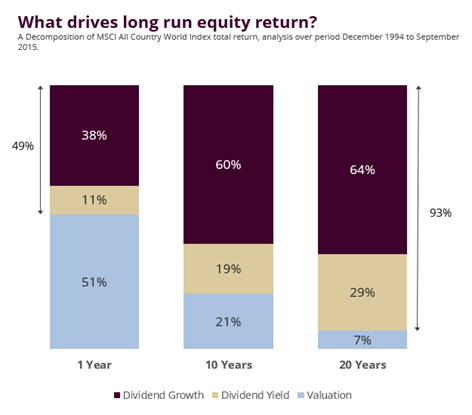

Dividend Growth – Accounts for a large proportion of long-term total returns

In addition to the above, evidence suggests that companies who grow their dividends over the long term also perform better on a total return basis than non-dividend growers. We may have highlighted this before, though this seems a suitable time for a reminder.

Dundas Global Investors, managers of the Heriot Global fund, for which dividend growth is a core part of their investment philosophy, brought the following study to our attention: MSCI 2016 study of long-term return on behalf of the Norwegian Ministry of finance:

‘As the investment horizon increases, the fundamentals (namely, dividend yield and dividend growth) become the dominant sources of performance, explaining more than 90% of total equity returns over 20 years.’

Another point not to be missed, which I think is very prevalent in markets right now, is that over shorter time frames (see above 1 year), you are at the mercy of Mr Market with valuations changes having a great effect on returns.

However, if you ignore short-term noise and act as long-term investors (which our managers and we are), valuation changes play much less of a role with the strength of these company fundamentals dictating returns with dividend growth/ dividend yield explaining 79% of returns over a 10-year period and 93% over 20 years.

Inflation: Highlighting companies who can grow dividends above inflation

Dividend growth is the core strategy employed by both Heriot Global and Fidelity European funds but is also relevant to our Equity Income managers, who typically have higher starting yields but have also been able to grow dividends. Below are a few of our Equity Income managers we have met recently.

Unicorn UK Income: Dividend Compound Annual Growth Rate (CAGR) of 5% since launch

Artemis Global Income: Distribution CAGR of 7% from 2012-2020

Franklin Templeton Global Infrastructure: CAGR of 5.7% per annum since launch

We can all agree that inflation (9.1% in the UK and 8.6% in the US) will soon peak (base effects if nothing else) but also settle at a figure higher than the two per cent we have been used to seeing over the last decade.

In reference to the above, if you can employ managers who are able to grow dividends above inflation, I think this will be a very powerful story for investors and potentially lead to further inflows and subsequent upwards rerating of these companies.

In this environment of higher interest rates (Central Bank response to inflation), I believe those managers who focus less on the fundamentals and rely on future growth (especially if companies are profitless) will continue to struggle in relative terms. As Dario Perkins, Managing Director, Global Macro, at TS Lombard states:

‘We are calling the 2020s the “Tangible 20s” because, in what is no longer an era of permazero interest rates and QE, investors will need greater exposure to the real economy rather than just long-duration tech stocks. Value equities performed relatively well in the 1940s and 1970s and are likely to comfortably outperform growth stocks in this new macro regime.’

Fixed Income performance

On the income theme, as mentioned earlier in the piece, Tideway uses Fixed income funds to generate a core engine of yield in investor portfolios.

It has been a rocky ride for all asset classes in 2022, though mainly in fixed income markets with lower risk status. Most notably, gilts, seen as risk-free investments, have been one of the worst-performing asset classes. Despite the short-term pain in portfolios, we do not think it is all bad news for fixed income.

Higher Forward-Looking Returns in Fixed Income

In the high yield and hybrid capital markets, most returns come from yield rather than capital appreciation, especially when rates are static. We can therefore use these yields as a good proxy for forward-looking returns whilst accounting for some defaults.

Despite the short-term pain seen this year, with rising yields and widening spreads, fixed-income investors are better compensated in this new macro environment with yields in excess of where we believe inflation will settle at.

These higher yields can be illustrated by the yields on our fixed income managers below. Furthermore, those funds that can reinvest at higher rates quickest (short duration) should also rebound the fastest (think Sanlam Credit and Artemis Short Dated Global High Yield).

An overview of our current fixed income managers:

- Sanlam Hybrid Capital: 6% (31/05/2022) Yield to Worst (YTW)

- Sanlam Credit: 5.2% (31/05/2022) YTW

- Royal London Sterling Extra Yield: 6.08% (31/05/2022) YTW

- Artemis Short Dated Global High Yield: 7.1% (30/06/2022) YTW

- Artemis Corporate Bond: 4.1% (30/06/2022) YTW

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing

At Tideway, we deliver a first-class service, and our clients’ referrals have allowed us to grow our business. If you are an active advocate for Tideway and would like to benefit from referring your friends, colleagues, or associates, do make sure you sign up for our referral scheme here.