At our last investment committee meeting, we noted that the numbers of funds in our portfolios had been steadily creeping upwards as we had added a few new managers in recent months . Too many managers and you may as well hold the index, too few and you can be over exposed to a particular style of company or bond heavily favoured by one manager.

The meeting held on the 21st July also noted few key themes;

- We are probably not out of the woods on inflation. Whilst we could see commodity prices falling and expectations that peak inflation may already be close or even behind us, there was a strong view it might not be so easy to contain and certainly tough to get it down to 2% targets from current levels.

- The US economy looks in better shape than UK and Europe. This may be illusionary but as is often the case the US economy looks more dynamic and likely to avoid any major recession.

- The removal of quantitative easing (QE) setting the agenda. TS Lombard’s Martin Shenfield showed us some strong graphical evidence of the impact of the removal of quantitative easing which primarily involves depressing bond yields through Central Bank buy backs on bond yields and equity values – there is more quantitative tightening (QT) to come was the view.

We generally felt we were well positioned both in our bond funds and equity funds for current conditions and noted the relatively strong recovery under way. However, with the themes above in mind we challenged Nick Gait our investment director to reduce the number of funds held, particularly our equity funds.

The recovery has continued and US consumer price indices did indeed drop this month suggesting peak inflation may have passed but the Bank of England continued to raise base interest rates. UK gilt yields which had started to fall in late June and July are rising again.

The main ones for me were:

- To sell our Ballie Gifford Global Alpha fund in favour of Heriot Global and Fidelity US Special situations. Topping up two managers who we feel pay more attention to the valuation of companies than Ballie Gifford, who of course did spectacularly, but then quite badly in the Covid tech boom and bust.

- To increase our US weightings. We were significantly underweight US equities in 2018 which cost us, since then we have been steadily increasing and now we are pretty much on benchmark. We are though not hugging the index which is still dominated by big US tech.

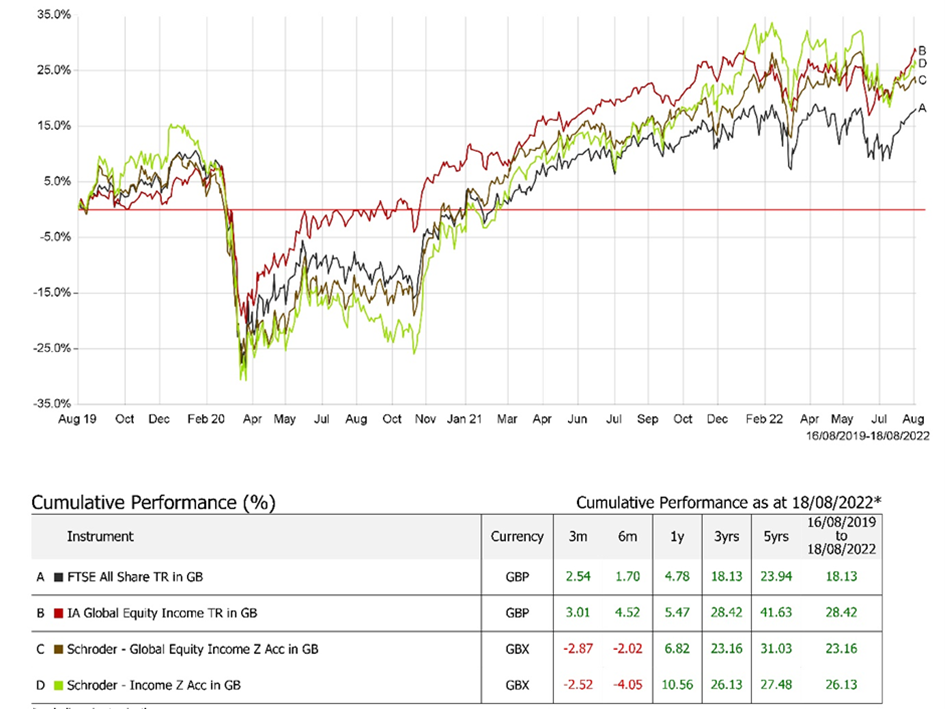

For those like me who like a picture, here below is the recent performance of the three funds in question over the last three years versus the world index.

Spookily the three-year returns of both the Fidelity and Heriot fund are very similar to the index, but the pathways to that point are very different with Fidelity a more value orientated manager and Heriot looking for quality dividend growth. Ballie Gifford’s fall hurt more than its gains and we feel there is still some vulnerability given the themes above.

Nick explains in more detail below.

Nick Gait

Following last month’s investment committee meeting we have sold the full positions in long time holdings Schroder Income (United Kingdom) and Baillie Gifford Global Alpha.

The proceeds of these sales were addedto existing high conviction positions in Schroder Global Equity Income, Heriot Global and Fidelity American Special Situations.

Rationale summary:

Since the beginning of the global pandemic, we have added several new Equity funds to Multi Asset portfolios; Montanaro Better World, Fidelity Asia Pacific Opportunities and Fidelity American Special Situations.

Rather than making corresponding sales we reduced other position sizes and blended with existing positions. For example, most recently we opened a position in Fidelity American Special Situations as we wanted to increase our exposure to the US, whilst having more valuation constraint than our existing more growth orientated manager provided, Artemis US Select.

With these three additions and lack of sales we were conscious that our holdings were becoming more diluted. We have made these latest changes to ensure that our investors benefit should our highest conviction positions outperform.

We continue to like both strategies that we have sold; Schroder Global Equity Income, one of our highest conviction positions, contains many of the top holdings in Schroder Income whilst Baillie Gifford Global Alpha remains a holding in our specialist Equity growth portfolios.

The managers have done nothing wrong, we simply felt we had better alternatives already in the portfolio. We now have eleven specialist Equity funds in our multi-asset portfolios and are currently happy with this number: We think this provides adequate diversification without hindering our portfolio’s ability to outperform the broader equity market.

Geographical allocations were also considered when making these changes with our desire to increase our exposure to US (Fidelity American Special Situations), which we started doing in H1 this year, whilst reducing our overweight to the UK (Schroder Income).

Portfolio Change: Sell Schroder Income (UK Value) / Add to Schroder Global Equity Income (Global Value):

- High crossover with Schroder Global Equity Income which is run by the same investment team and adheres to the same investment process with many of the highest conviction picks in the UK portfolio also contained in the Global portfolio.

- Global Equity Income is a best ideas funds with no constraint on the investment universe from which to the manager can select the absolute best companies to fit their value strategy. The UK vehicle is constrained by country of listing.

- In isolation, and theoretically speaking the UK Income version of the strategy would be the best allocation of capital if the Global strategy were to contain a 100% allocation to the UK. This figure is at 20% (June Factsheet) but has been much higher in the past.

- The presence of foreign holdings in UK fund (prospectus allows a limited allocation to companies not listed in the UK) also would seem indicate that the best opportunities are not all in the UK.

- Future portfolio geographical exposure will be more dynamic as the manager turns the portfolio looking for the best investment opportunities.

- Helps to reduce overweight to UK in line with committee latest views

Portfolio Change: Sell Baillie Gifford Global Alpha/ Add to Heriot Global:

- Baillie Gifford Global Alpha has been held in model portfolios since 2017 and over the period has been one of our top performers despite relative underperformance to the growth style of investing in 2022 due to macro headwinds.

- Even though we would have sold at a loss for any investors purchasing this year, most of these proceeds have been reinvested into Heriot Global, also in negative territory in this period (though Heriot has slightly outperformed). We were also able to sell into the strength of the recent equity market rally of which the growth funds led.

- Numbers game referred to earlier with our preference for capital to go to higher conviction strategies. Both funds invest in global growth companies though the investment processes are markedly different along with the types of growth company the managers look for.

- We believe Heriot’s dividend growth strategy will be more suited to times ahead; focus on sustainable growth of dividends to deliver returns rather than relying on valuation re-ratings which some of the more rapid growth names that Baillie Gifford’s Global Alpha invest in, rely upon.

- More conservative strategy which we believe will stand portfolios in better stead through volatile times whilst delivering competitive long-term returns. We believe the strategy is better suited in a world of higher inflation and interest rates.

Add Fidelity American Special Situations:

- The switches mentioned above were not exactly one for one. Schroder Income and Baillie Gifford accounted for 40% and 60% of the proceeds with reinvestment into Schroder Global Equity income and Heriot Global at 30% and 42% respectively. The balance of 28% went to Fidelity’s American Special Situations strategy.

- Replacing some value exposure lost in the sale of Schroder Income

- Further closes some of US Equity underweight – With an offering cheaper than the wider US market, should provide some additional protection should broader valuations re-rate downwards.

- Emphasis on quality businesses, in addition to being strict on valuations, should help should inflation continue to be a problem. Quality businesses are more able to pass costs on to the end consumer.

Portfolio Positioning:

We have remained stylistically neutral across the Equity book owning a roughly equal weighting of those who adhere to the growth style of investing and the value school of investing for whom starting valuations are most important (according to Morningstar’s style box).

This should stand us in good stead should growth and value keep taking turns in leading markets (reduces portfolio volatility). We have also maintained a strong balance between higher dividend yields and lower dividend yielders in the portfolio (including dividend growth).

Fixed income positioning remains unchanged with valuations now looking relatively attractive versus Equities in our opinion post the recent Equity market rally (there has not been a rally in Credit to the same extent).

We believe our fixed income positions will provide more protection than equities should there be no safe landing in economies, whilst providing investors with a high income if the markets go sideways. At these current levels of yield, we are happy to simply wait and clip the coupons.

If you’re interested in reading more about our market updates visit our Insights and News.

- The content of this document is for information purposes only and should not be construed as financial advice

- Please be aware that the value of investments, and the income you may receive from them, cannot be guaranteed and may fall as well as rise

- We always recommend that you seek professional regulated financial advice before investing