At Tideway we often talk about retirement in three phases; the first being the early years in retirement or ‘active years’ where you may have more time and enjoy good health. Typically, this is the time you enjoy as you are no longer working and may have additional costs to support this new lifestyle.

The second phase is known as the ‘passive years’, as you start to move into older age and your ability and desire to travel or undertake hobbies reduces. You may find that you settle into a quieter and more sedate lifestyle. The final stage or ‘last years’ phase has the potential to be a very expensive with nursing care costs and other medical needs.

Clearly spending patterns change as an individual moves through the course of their retirement, but there is one constant throughout and these are your basic living costs. These are often referred to as core needs and, in short, are your essential expenditures that must be met to ensure you keep the roof over your head and maintain a minimum standard of living. Therefore, the starting point in understanding what your income requirements are in retirement will be to calculate your household costs. You will need to ask yourself how much your utility bills are, how much do you spend in the supermarket and do you have any financial liabilities that must be met. Keeping a record of what you spend each month is key to understanding this figure.

You should also consider your lifestyle costs which are the things that are important to you and don’t want to give up. For example, eating out, going to the cinema, gym membership, holidays etc. These costs will vary significantly throughout the phases of retirement. Perhaps consider the first 5-10 years where you might want to spend more time travelling and on active hobbies. Luxury items may be an additional requirement for some.

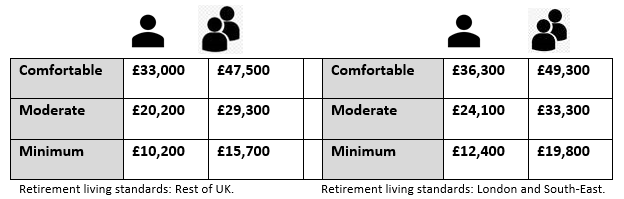

The Pension & Lifetime Savings Association (PLSA) ‘Retirement Living Standards’ (RLS) report October 2019, suggested that average minimum income needs in retirement, for a couple and a single person, are as follows:

Now that you understand how to work out your basic and lifestyle costs, you should know how much is needed on a monthly and annual basis, net of tax. Remember that tax is still due, even in retirement!

You should now establish what you have in place in terms of pensions and retirement savings. Are there any secured benefits coming into payment, such as state pension or occupational pension scheme benefits? What other assets do you have that can help derive your income requirement? Will you continue to work on a part time basis?

To obtain a state pension forecast, you should follow the link below:

https://www.gov.uk/check-state-pension

Tideway’s drawdown calculator is designed to give you a good indication of a realistic income withdrawal rate, by allowing you to illustrate different scenarios and stress test the sustainability of your income. I have found this a useful tool when completing my annual reviews as it allows my clients a visual illustration of how long their funds are likely to last. The drawdown calculator works on a today’s money basis, therefore the figures that you enter do not need to be adjusted for inflation.

The calculator can be found using the link below:

https://www.tidewaywealth.co.uk/drawdown-calculator

If you are interested to know more about this area of financial planning, please contact your Wealth Adviser or book in an initial free of charge guidance session; we will be happy to discuss your options.

Tideway recently sent out a client expenditure email asking clients to kindly update us on their expenditure in retirement so if you have not already done so, please update your details via the portal and this can be factored in your next review.