An actively managed fund is typically more expensive than a passive managed fund. You pay for a fund manager who will pick and choose the investments to include in their fund based on their expertise and analysis. A passive managed fund tracks the market so is by definition cheaper.

If you start Googling which is better, active versus passive investing, you will be entering a huge debate with articles supporting both sides. The pro-passive article says you should go passive because a lot of active managers fail to hit their benchmarks after fees. The pro-active side say why accept average?

For a novice investor it can be a real can of worms and lot companies use this to the advantage quoting high performance numbers and hiding the cost or the other way around, quoting low costs but masking a poor solution. This is a marketing ploy, which, I have to say, I don’t agree with.

At Tideway, as you know, we largely choose active managers but we don’t have an aversion to passive.

Our flagship multi-asset portfolios, which we call our ‘Stable Return Portfolios’ target an outcome with capital preservation and income high on the priority list, regardless of which risk strategy you take or can tolerate with us. We clearly want to provide our client’s their desired return after fees in a ‘Stable’ manner and often we are dealing with irreplaceable capital for individuals.

As our investors know, these portfolios have an allocation to fixed income funds, rather than traditional stock broking method of focusing on equities. Whilst fixed income funds are certainly not risk free, what they do provide is much more predictable returns and stability than the riskier equity counterparts. Fixed income bonds rely on a company being able to meet its obligations rather than making a profit, or not, like an equity.

The case for using active or passive fixed income portfolio isn’t really up for debate. Passive investing often uses capitalization, meaning you have a higher exposure to the larger companies on the equity side but with fixed income you have a higher exposure to the companies with the most debt. That doesn’t seem like a sound investment to me. You also have a mix-match of liquidity between fixed income and passive funds meaning you are not always getting the best price, and instead are actually having to pay on the ‘spread’ i.e. the difference between the buying and selling price, every time someone else goes in and out of the fund.

Some fixed income funds may also fail to pay their debt, known as defaulting, and by hiring an active manager experienced and knowledgeable about the fixed income market you can hopefully remove some of this risk by avoiding specific companies and bonds.

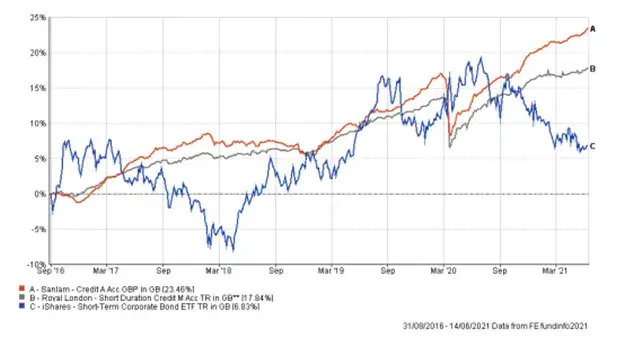

See below a graph that shows difference of Tideway’s top two short dated fixed income fund picks since 2016 against a large passive ETF tracker over the same period. Which one is not providing a Stable Return?

When you move into equites there is a case for passive investing if you are investing in large markets and happy ride the volatility. Considering the historical performance of equities, the chances are, over the long term, you will make a good return; however this can never be guaranteed.

Whilst the total return of these passive funds can be desirable, there is often little yield and a lot of our investors aren’t prepared, or able, to ride market volatility with their irreplaceable capital. The horizon planning can also help take sequencing risk out of the equation i.e. taking money out at the wrong the time and failing to recover.

It is also worth noting that within passive management you get a bit of everything so you cannot pick and choose your investments easily. Ethical stances, taking a certain theme or style that you might believe will add to the portfolio has to be taken as a whole. You do get a lot of the good with capitalization, but you also get the bad too.

At Tideway, we agree that not all fund managers are worth paying for but there are certainly some and it is our job to find them, analyze them, monitor them and move them in and out of the portfolio at a time we most see fit. If there does come a time when a passive fund is worth having and we cannot see a reason to justify the additional cost of a fund manager then we will save you the money and go passive (we have done it in the past). It is always our priority to do what is best for our clients as we look to build long term relationship.

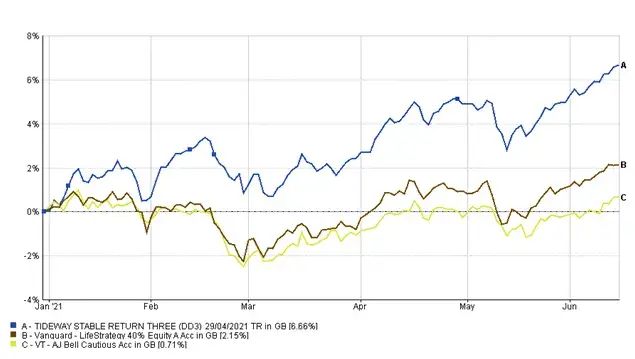

So, I guess I need to answer the question: is our use of active management working? I have produced a graph below that shows the return of our Stable Return 3 (medium risk) in 2021 which has a 40% exposure to equity funds against two larger passive providers which have a similar level of equity exposure and so a fair comparison on a risk rated basis. Note these returns are after the associated active or passive fund fee. Which return would you prefer?

If you are interested to know more do get in touch with your Wealth Adviser or book in an initial free of charge session with one of our Chartered Advisers who will happily talk you through. At Tideway we have a number of experienced Chartered Financial Planners and Wealth Advisers who can work together for you and find an appropriate solution based on your personal circumstance.